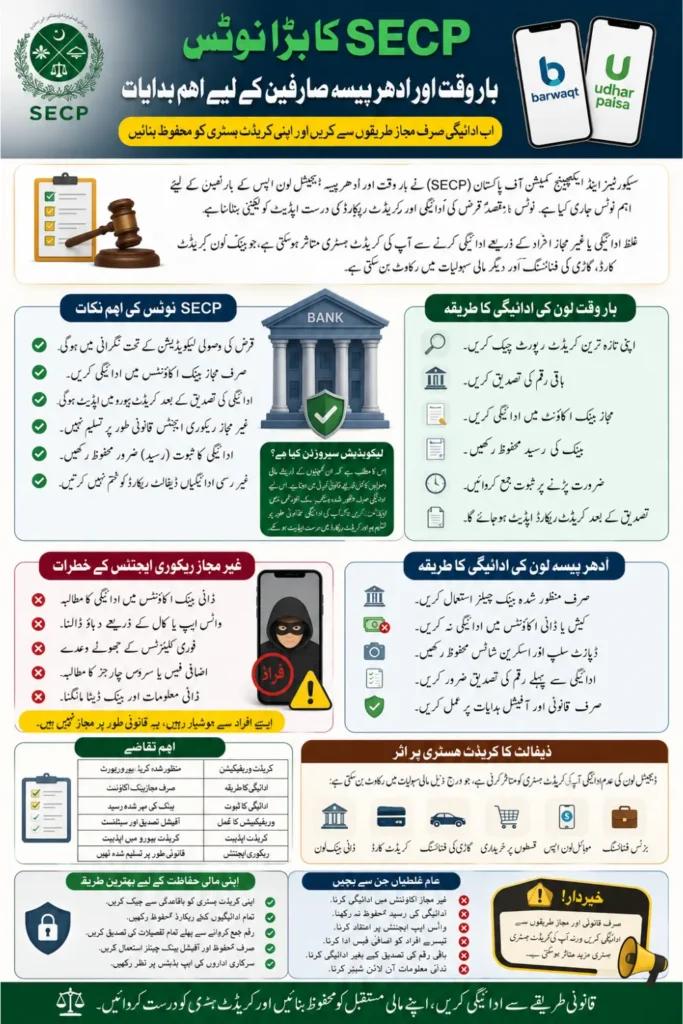

The Securities and Exchange Commission of Pakistan (SECP) has issued an important notice for users of Barwaqt and UdharPaisa digital loan applications in Pakistan. The notice mainly focuses on repayment procedures, liquidation supervision, and proper credit record updates for borrowers who still have pending loan balances.

Many users are facing problems because unpaid digital loans continue appearing in their credit history. These negative records can create difficulties when applying for bank loans, credit cards, vehicle financing, or future digital lending services. SECP has clarified that repayments must now follow official legal channels only to ensure transparent settlement and accurate credit reporting.

Why SECP Issued Notice for Barwaqt and UdharPaisa Users

SECP regulates non-banking financial companies and digital lending services in Pakistan. After regulatory action against companies linked with Barwaqt and UdharPaisa, many borrowers became confused about how to clear their pending loans properly.

You can also read: BISP Nashonuma Registration

To prevent fraud and misuse, SECP introduced a structured repayment framework. The notice ensures that borrowers use only authorized bank accounts and verified liquidation channels instead of unofficial recovery agents or social media claims.

Key Points Highlighted in the SECP Notice

- Loan recovery is supervised under liquidation proceedings

- Only designated bank accounts are legally approved

- Credit bureau updates happen after payment verification

- Unauthorized recovery agents are not recognized

- Borrowers must keep proof of all payments

- Unofficial settlements may not remove default records

This system helps protect borrowers from scams while maintaining accurate financial records.

What Does Liquidation Supervision Mean?

Liquidation supervision means the companies behind these digital loan apps are operating under legal financial settlement procedures. In such cases, repayment collection is monitored officially to ensure fairness and proper record management.

For borrowers, this means loan payments cannot be sent randomly to personal accounts, agents, or mobile wallet numbers shared online. Payments must follow the approved banking process so that the settlement becomes legally valid and visible in Pakistan’s credit reporting systems.

Barwaqt Loan Repayment Process Explained

Barwaqt users who still have unpaid balances should first verify the exact outstanding amount through official records or credit reports. This helps avoid overpayment or disputes during settlement.

After confirmation, borrowers must deposit the repayment amount into the officially assigned bank account. The bank-stamped receipt should be kept safely because it acts as legal proof of payment during credit record verification.

Steps to Clear Barwaqt Loans

- Check your latest credit report

- Confirm pending dues through official channels

- Deposit payment into the designated bank account

- Keep original payment receipts safely

- Submit proof if verification is requested

- Wait for official credit record update

Once the process is completed successfully, the default status may gradually be updated in the credit system.

UdharPaisa Loan Settlement Procedure

The repayment procedure for UdharPaisa users is similar under SECP supervision. Borrowers must avoid paying through unofficial methods because only verified payments are recognized during liquidation.

Users should carefully match their outstanding loan amount with official records before making payment. Any mismatch or incorrect transaction can delay credit history correction and future loan eligibility restoration.

Important Requirements for UdharPaisa Borrowers

- Use only approved bank payment channels

- Avoid cash handovers to private agents

- Keep deposit slips and screenshots securely

- Verify settlement details before payment

- Follow only official instructions from legal authorities

Proper documentation is important because banks and credit bureaus rely on verified records for updating financial history.

Risks of Unauthorized Loan Recovery Agents

One major issue in Pakistan’s digital lending sector is fake recovery activity. Many borrowers receive WhatsApp calls, SMS messages, or social media requests from individuals claiming they can instantly clear loan records.

SECP has clearly warned users that such individuals are not legally authorized. Payments made through unofficial channels often fail to update credit records and can result in financial fraud.

Common Warning Signs of Fake Recovery Scams

- Requests for payment to personal bank accounts

- Pressure tactics through WhatsApp or calls

- Extra “service charges” for quick clearance

- Promises to instantly remove default history

- Requests for sensitive banking information

Borrowers should immediately avoid suspicious recovery requests and rely only on official channels.

You can also read: BISP 8171 SMS Not Working 5 Easy Fixes

How Digital Loan Defaults Affect Credit History in Pakistan

Digital lending platforms share repayment data with national credit databases used by banks and financial institutions. If a borrower fails to repay loans properly, the unpaid balance may remain visible as a default.

Negative credit records can affect financial opportunities for several years, especially for people planning to apply for formal banking products or financing facilities in the future.

Financial Services Affected by Bad Credit Records

- Personal bank loans

- Credit card approvals

- Car and motorcycle financing

- Installment-based purchases

- Future mobile lending applications

- Business financing options

Clearing outstanding dues through official procedures helps improve financial credibility over time.

Official Loan Clearance Requirements

| Category | Requirement |

|---|---|

| Credit verification | Approved credit bureau report |

| Payment method | Assigned bank account only |

| Proof of payment | Bank-stamped receipt |

| Verification process | Official settlement confirmation |

| Credit update | Verified entry in credit database |

| Recovery agents | Not legally recognized |

This process improves transparency and reduces the risk of duplicate or fake recovery claims.

Common Mistakes Borrowers Should Avoid

Many users create additional problems by following incorrect repayment methods or trusting unofficial information online. Even small mistakes can delay credit record updates for months.

- Paying through unofficial bank accounts

- Ignoring payment receipts after settlement

- Trusting random WhatsApp recovery agents

- Paying extra fees to third parties

- Failing to verify outstanding balances

- Sharing personal financial details online

Avoiding these mistakes can help borrowers complete settlements safely and correctly.

Best Practices to Protect Your Financial Record

Borrowers should regularly monitor their credit history and keep proper records of all loan transactions. This is especially important as Pakistan’s digital finance sector continues expanding in 2026.

Helpful Financial Safety Tips

- Check your credit history regularly

- Save digital and physical payment records

- Confirm repayment details before depositing money

- Follow updates from official regulatory sources

- Avoid unofficial settlement shortcuts

- Use secure banking channels only

Maintaining accurate records helps reduce future disputes and improves long-term financial stability.

You can also read: BISP 2027 Update 19500 Payment

Latest Update About Digital Loan Apps in Pakistan 2026

The Pakistani financial sector is moving toward stronger regulation of digital lending platforms. Authorities are increasing monitoring to improve borrower protection, reduce harassment complaints, and ensure transparent loan recovery systems.

SECP’s latest notice shows that regulators are focusing more on legal repayment structures, verified recovery procedures, and proper credit reporting. Borrowers are now expected to follow official banking methods instead of informal settlements commonly used in previous years.

Frequently Asked Questions (FAQs)

Can Barwaqt or UdharPaisa loans be paid through Easypaisa or JazzCash?

No. SECP has emphasized that repayments must only be made through officially designated bank accounts.

How long does it take to update the credit record after repayment?

Credit updates may take several weeks after successful verification and processing by the liquidation authorities.

Are WhatsApp recovery agents officially approved?

No. SECP has clearly stated that unofficial recovery agents are not legally authorized.

Will unpaid digital loans affect future bank financing?

Yes. Outstanding digital loan defaults can impact eligibility for loans, credit cards, and financing services.

Is keeping the payment receipt necessary?

Yes. Bank-stamped receipts act as proof of settlement and may be required during verification.

You can also read: Holidays on the Occasion of Eid

Conclusion

The SECP Barwaqt UdharPaisa notice in Pakistan highlights the importance of using official repayment procedures for digital loan settlements. Borrowers should avoid fake recovery agents, unauthorized payment methods, and misleading online claims that may create additional financial problems.

Following the approved banking process helps borrowers clear outstanding dues legally and improves the chances of correcting negative credit records. As Pakistan strengthens regulation of digital loan apps in 2026, using verified channels and maintaining proper documentation has become more important than ever for financial security and future banking access. SECP Barwaqt Udharpaisa Notice